|

Property Makler

Advanced analytics for residential real estate investing |

|

Dubai, UAE US |

Dubai US Market Research

Dubai apartment investment market, 2024 results - price trends, emerging hotspots, and market challenges

23 Jan 2025

Key points

- Luxury areas mixed performance: Premium neighborhoods like Palm Jumeirah and Downtown Dubai showed modest price growth or declines, with sales volumes falling due to affordability challenges and market saturation. Emerging areas driving growth: Affordable locations such as Hessyan 1, International City Phase 1, and Town Square saw significant price increases and rising demand, reflecting their appeal to value-conscious buyers.

- Off-plan sales dominance: Areas like Dubai Creek Harbour and Town Square continue to thrive with high shares of off-plan sales, supported by flexible payment plans and the allure of new developments.

- Mid-tier markets resilience: Communities like JVC and Dubai Studio City showed strong price and sales growth, benefiting from strategic locations and demand for budget-friendly yet modern properties.

- Challenges in certain areas: Business Bay and Al Quoz 4 faced declining sales volumes, highlighting potential oversupply or reduced buyer interest in these markets.

Overview of market dynamics in 2024

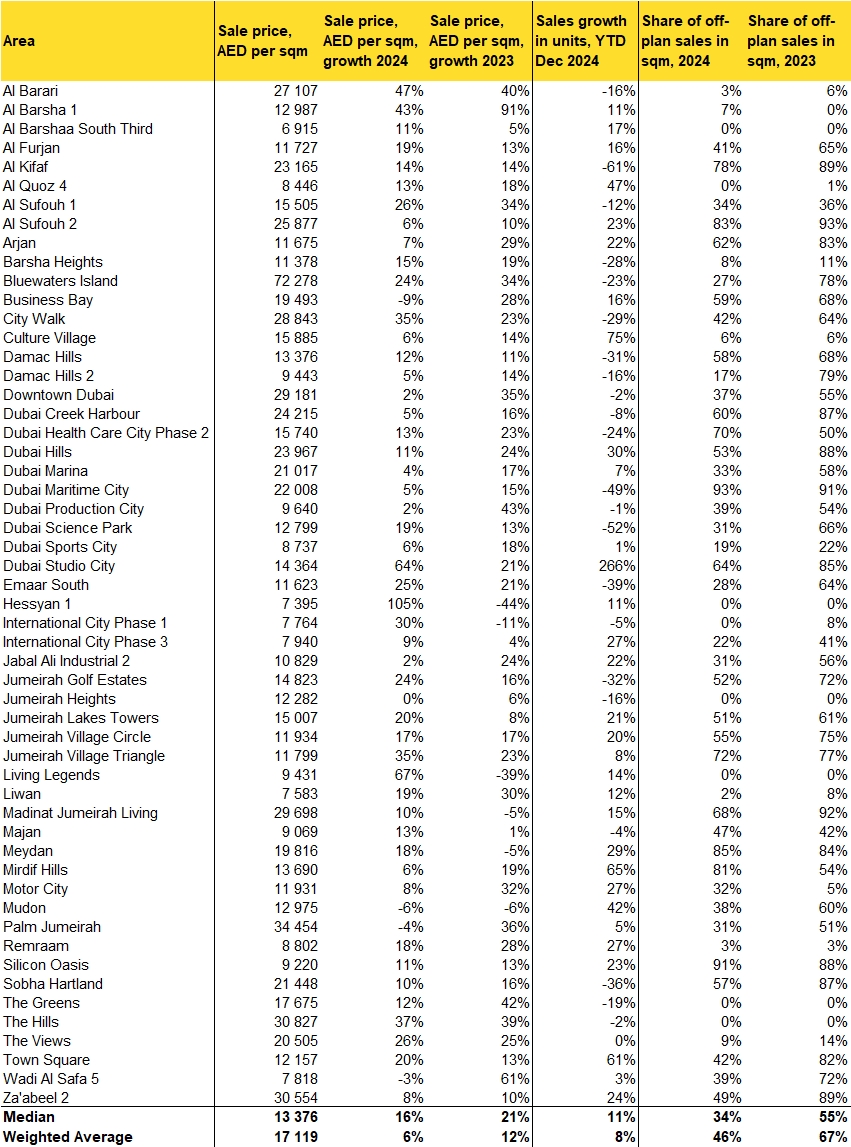

The Dubai residential apartment market in 2024 continued to hold the leading global position as the leading growing real estate market attracting capital globally: weighted average prices increased 6% while volume increased 8%. The market exhibited mixed trends across different areas, reflecting varied buyer preferences and market dynamics. Overall, the weighted average sale price per square meter have reached AED 17,119, highlighting steady demand in the city’s diverse property landscape.Key Insights from 2024 Price Changes

Prime locations like Downtown Dubai and Dubai Hills recorded minimal growth at 2% and 5%, respectively. This moderation could be due to market saturation or shifting demand toward emerging neighborhoods with better value propositions. Central locations for lower budgets like Business Bay saw a price decline of 9% while volume increased 16%. Active new construction while continuing traffic jams and distance of many buildings from the metro lead to these dynamics. Several areas have experienced significant price growth such as International City Phase 1 (30%) and Jumeirah Golf Estates (24%), attracting buyers looking for affordability or luxury.Sales Volume and Price Correlation

An inverse relationship between price growth and sales growth is evident in several areas. For example, Al Barari and Jumeirah Golf Estates, with price increases of 47% and 24%, respectively, saw declines in unit sales at -16% and -22%. Such trends suggest that sharp price hikes might deter buyers, reducing transaction volumes. Interestingly, Dubai Studio City bucks this trend, recording a remarkable 266% growth in unit sales alongside a substantial 64% price increase. This anomaly indicates that certain locations can sustain high demand despite rising prices, likely due to new project launches or enhanced amenities that appeal to buyers.The Role of Off-Plan Sales

Off-plan transactions remain a dominant force in the Dubai apartment market, with 46% of total sales attributed to off-plan units in 2024. Areas like Dubai Creek Harbour (85%) and Town Square (61%) continue to attract buyers, reflecting the appeal of modern developments and flexible payment plans. However, this is a slight decline compared to 2023, where off-plan sales accounted for 57% of total transactions.Area-specific trends in Dubai's residential apartment market for 2024

Luxury Areas and Premium Locations

Premium areas like Al Barari, Downtown Dubai, and Palm Jumeirah continue to hold their appeal, but they display mixed performance in 2024. Al Barari saw a significant price increase of 47%, reaching AED 27,107 per square meter, despite a 16% decline in unit sales. Similarly, Palm Jumeirah, with one of the highest sale prices at AED 34,475 per square meter, experienced a 6% price drop and a substantial 42% decline in sales volumes. These trends highlight affordability constraints and potential market saturation in ultra-luxury locations.Downtown Dubai, a hallmark of Dubai’s luxury market, recorded a modest price increase of 2%, while sales volumes contracted by 2%. This performance suggests that while Downtown remains a preferred choice for investors, buyer activity may be shifting toward more affordable or emerging areas.

Emerging Areas and Affordability-Driven Growth

Emerging areas like Hessa 1 and International City Phase 1 witnessed significant growth in sale prices, reflecting their rising popularity among buyers. Hessa 1 recorded a staggering 1050% price increase, albeit with a 44% decline in unit sales, indicating limited supply or selective demand driving prices upward. Meanwhile, International City Phase 1 saw a 30% rise in prices with a marginal 5% decline in unit sales, showcasing its strong position as a value-driven market. Other affordable areas, such as Town Square, experienced a balanced market with a 20% price increase alongside a robust 61% growth in unit sales. This demonstrates the sustained appeal of budget-friendly developments that cater to middle-income buyers and young families.Mixed Performance in Mid-Tier Markets

Mid-tier markets like Dubai Hills, Jumeirah Village Circle (JVC), and Dubai Studio City showed resilience with steady price growth and mixed sales performance. Dubai Hills saw a moderate 5% price increase but suffered a 49% decline in unit sales, potentially reflecting challenges in attracting buyers despite its premium offerings. JVC, on the other hand, recorded a 17% price increase and a 20% rise in unit sales, indicating robust demand fueled by its strategic location and competitive pricing. Meanwhile, Dubai Studio City defied broader trends, with both a 64% price increase and a remarkable 266% surge in unit sales, suggesting a successful influx of new developments and strong buyer interest in this up-and-coming community.High Demand for Off-Plan Projects

Areas with high shares of off-plan sales, such as Dubai Creek Harbour (85%) and Town Square (61%), underline the growing buyer preference for modern, future-ready properties. These neighborhoods are benefiting from flexible payment plans and the appeal of new developments, making them hotspots for investors and first-time buyers alike.Areas Facing Market Challenges

Some areas have struggled in 2024, with declining prices and sales volumes. Business Bay, a central business district, saw a 9% drop in prices and a 28% decline in sales volumes, signaling waning demand in this once-thriving area. Al Quoz 4, another area facing headwinds, recorded a 13% price increase but a steep 47% drop in unit sales, indicating potential oversupply or a lack of competitive offerings.Challenges facing Dubai's residential apartment market in 2024

Despite steady overall growth, the Dubai residential apartment market in 2024 faced several challenges impacting certain areas and buyer segments:- Affordability Constraints in Luxury Areas: Premium locations like Palm Jumeirah and Downtown Dubai saw declining sales volumes, with Palm Jumeirah experiencing a 42% drop in unit sales despite its global appeal. High prices and limited affordability for many buyers have restricted activity in these ultra-luxury markets.

- Market Saturation in Established Neighborhoods: Areas such as Business Bay and Dubai Hills exhibited slow or negative price growth, coupled with significant sales declines of 28% and 49%, respectively. This suggests that increased competition or oversupply in these areas may be limiting their attractiveness to buyers.

- Shifts in Buyer Preferences: The decline in demand for ready-to-move-in properties in favor of off-plan developments has left some secondary market areas struggling to maintain transaction volumes. This shift highlights the importance of competitive pricing and modernized offerings to attract buyers.

- Economic and External Factors: Rising interest rates and global economic uncertainty pose additional risks, particularly for buyers reliant on mortgages. These factors could dampen buyer activity and limit further price growth in certain segments of the market.

Outlook for 2025

Looking ahead, the Dubai apartment market is expected to remain resilient. Established premium areas like Palm Jumeirah and Downtown Dubai are likely to maintain steady price growth due to their global appeal and limited inventory. Emerging neighborhoods such as International City and Dubai Studio City will continue to attract buyers with their affordability and growth potential. The focus on off-plan sales is anticipated to grow, driven by innovative project launches and investor-friendly government policies, such as long-term residency visas. However, economic uncertainties and rising interest rates might pose challenges, particularly for end-users reliant on mortgages. Dubai's real estate market remains dynamic, offering opportunities for investors and end-users alike, with localized factors playing a critical role in determining market trends.Note: 2024 data is for the full year (January – December 2024)

Tags: Sales Prices

Property Makler © 2026 Contacts T&C About