|

Property Makler

Advanced analytics for residential real estate investing |

|

Dubai, UAE US |

Dubai US Market Research

Dubai apartment investment market in 2024 - cap rates grow as rental growth outpace property prices

25 Jan 2025

Key points

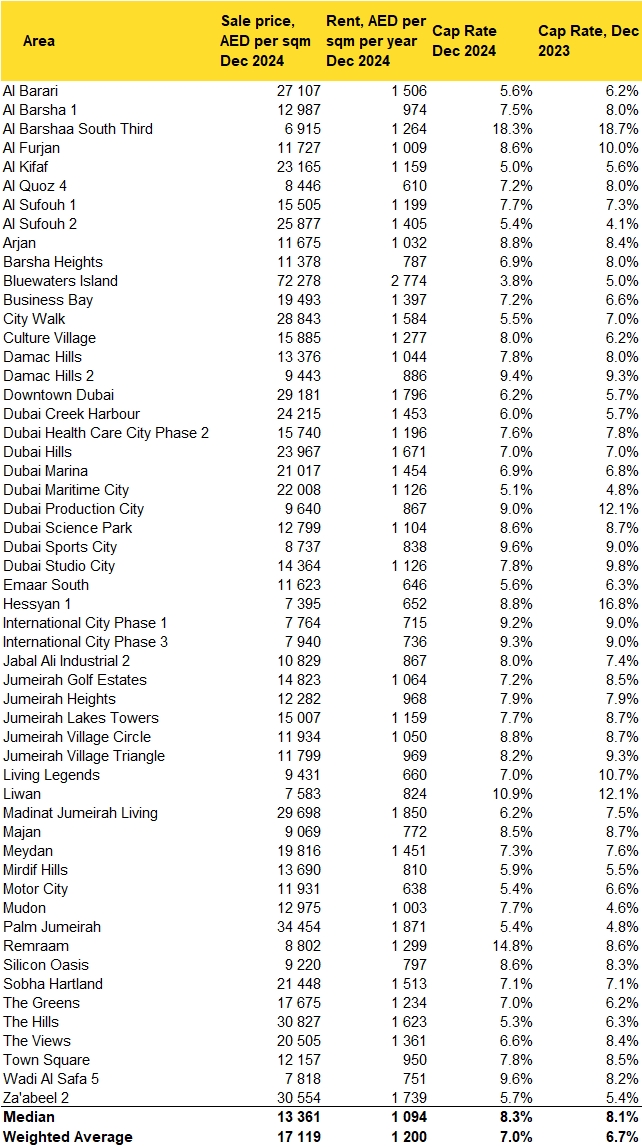

- Dubai's residential market saw an increase in sales prices and rental rates in 2024, with the weighted average sales price reaching AED 17,119 per sqm and rental rates at AED 1,200 per sqm per year.

- Cap rates increased slightly overall from 6.7% in December 2023 to 7.0% in December 2024, though prime areas saw declines due to rising property prices outpacing rental growth.

- High-yielding areas such as Remraam (14.8%) and Wadi Al Safa 5 (9.6%) gained investor interest, while luxury districts like Palm Jumeirah (5.4%) and Downtown Dubai (6.2%) saw stable demand.

- Dubai's market remains competitive globally, offering higher cap rates than prime markets like London and New York, while benefiting from a tax-free investment environment and strong economic fundamentals.

- Looking ahead to 2025, sales price growth is expected to moderate, cap rates may stabilize, and rental demand will remain strong, particularly in mid-tier and affordable housing segments.

Trends in Key Areas and Emerging Locations

Prime and Luxury Neighborhoods

Established high-end areas such as Downtown Dubai (6.2%), Palm Jumeirah (5.4%), and Bluewaters Island (3.8%) have seen moderate rental growth but significant increases in sales prices, resulting in lower cap rates compared to other segments. The decline in cap rates in these areas suggests a shift in investor preference toward higher-yielding districts, as rental yields have not kept pace with property appreciation. Conversely, some high-end locations such as Al Sufouh 2 saw an increase in cap rates from 4.1% in December 2023 to 5.4% in December 2024, reflecting stronger rental demand relative to sales price growth.Mid-Tier and High-Yielding Areas

Affordable and mid-income communities have consistently attracted investors due to their strong rental yields. Areas such as Jumeirah Village Circle (8.8%), Dubai Sports City (9.6%), and Silicon Oasis (8.6%) have maintained cap rates above the market average, making them favorable for investors seeking stable returns. Notably, Remraam has emerged as a key high-yielding area, with its cap rate surging from 8.6% in December 2023 to 14.8% in December 2024, driven by rapid rental growth. Similarly, Wadi Al Safa 5 recorded a strong cap rate of 9.6%, reflecting robust rental performance relative to sales price growth.Declining Cap Rates in Some Established Locations

Several traditionally strong investment areas have witnessed cap rate compression due to rising sales prices outpacing rental growth. For instance, Al Barari saw its cap rate drop from 6.2% to 5.6%, while City Walk experienced a decline from 7.0% to 5.5%. This suggests that investors in these locations are now prioritizing long-term capital appreciation over immediate rental yields.Factors Influencing Market Changes

Macro-Economic Factors

Dubai's economy has remained resilient in 2024, driven by continued growth in tourism, finance, and technology sectors. The influx of expatriates, coupled with high interest rates globally, has led to a strong rental market as more residents opt to rent rather than purchase homes. Additionally, government policies encouraging foreign investment and long-term residency visas have bolstered confidence in the real estate sector.Micro-Level Market Dynamics

The supply and demand balance has played a crucial role in shaping rental and sales price movements. While areas with new project deliveries, such as Dubai Hills and Dubai Creek Harbour, have experienced moderate rental increases, districts with limited new inventory have seen sharper price hikes. Investor sentiment has also shifted, with an increasing preference for high-yielding areas over traditional luxury investments. This has led to rising demand in areas such as Culture Village (cap rate up from 6.2% to 8.0%) and Al Sufouh 1 (cap rate up from 7.3% to 7.7%).Comparison with Other Global Cities

Dubai's investment market remains competitive when compared to other global real estate hubs. While prime locations in cities like London and New York have cap rates averaging 3% to 4%, Dubai’s luxury segment still offers better yields, with areas such as Downtown Dubai (6.2%) and The Hills (5.3%) providing higher returns. In contrast, emerging investment destinations such as Istanbul and Bangkok offer cap rates exceeding 8%, similar to Dubai’s mid-tier and affordable housing segments. However, Dubai’s tax-free environment, investor-friendly regulations, and strong economic fundamentals continue to attract global capital.Outlook for 2025

Moderation in Sales Price Growth

While Dubai's property market is expected to remain strong, sales price growth may moderate as affordability constraints limit further appreciation. Established prime areas are likely to see stabilized price levels, while high-growth mid-tier districts may continue to attract investor interest.Stabilization of Cap Rates

Cap rates are projected to stabilize in 2025, with less pronounced fluctuations as the market matures. While some high-yielding areas may see slight declines due to price appreciation, overall yields are expected to remain attractive relative to global benchmarks.Continued Demand for Rental Properties

With ongoing population growth and high borrowing costs discouraging homeownership, demand for rental properties is expected to stay robust. This will support rental price growth, particularly in areas offering affordability and modern amenities.Regulatory Developments

Potential policy adjustments by the Dubai Land Department (DLD) and Real Estate Regulatory Agency (RERA) could influence market dynamics. Expected measures such as enhanced rent control mechanisms and incentives for long-term investors may contribute to a more balanced investment environment.Conclusion

Dubai’s residential investment market has experienced significant transformations in 2024, with rising sales prices, stable to growing rental yields, and shifting investor preferences. While prime locations have maintained their allure, mid-tier and emerging areas have demonstrated superior cap rates and investment potential. Looking ahead to 2025, the market is expected to stabilize, offering opportunities for both capital appreciation and rental income growth in strategically selected locations.Note: 2024 data is for the full year (January – December 2024)

Tags: Cap rates, Investors

Property Makler © 2026 Contacts T&C About