|

Property Makler

Advanced analytics for residential real estate investing |

|

Dubai, UAE US |

Dubai US Market Research

Dubai apartment rental market in 2024 and outlook for 2025

24 Jan 2025

Key points

- Dubai's rental market saw strong growth in 2024, with mid-tier and affordable neighborhoods outperforming luxury areas in price increases.

- Prime locations like Downtown Dubai and Palm Jumeirah experienced slower but steady rental growth, while some high-end areas saw declining demand.

- Emerging residential hubs such as Remraam and Dubai Studio City attracted strong tenant interest due to affordability and modern infrastructure.

- Economic expansion, population growth, and high interest rates contributed to increased demand for rental properties.

- In 2025, rental prices are expected to moderate, with new supply and tenant migration towards affordable areas playing key roles in shaping the market.

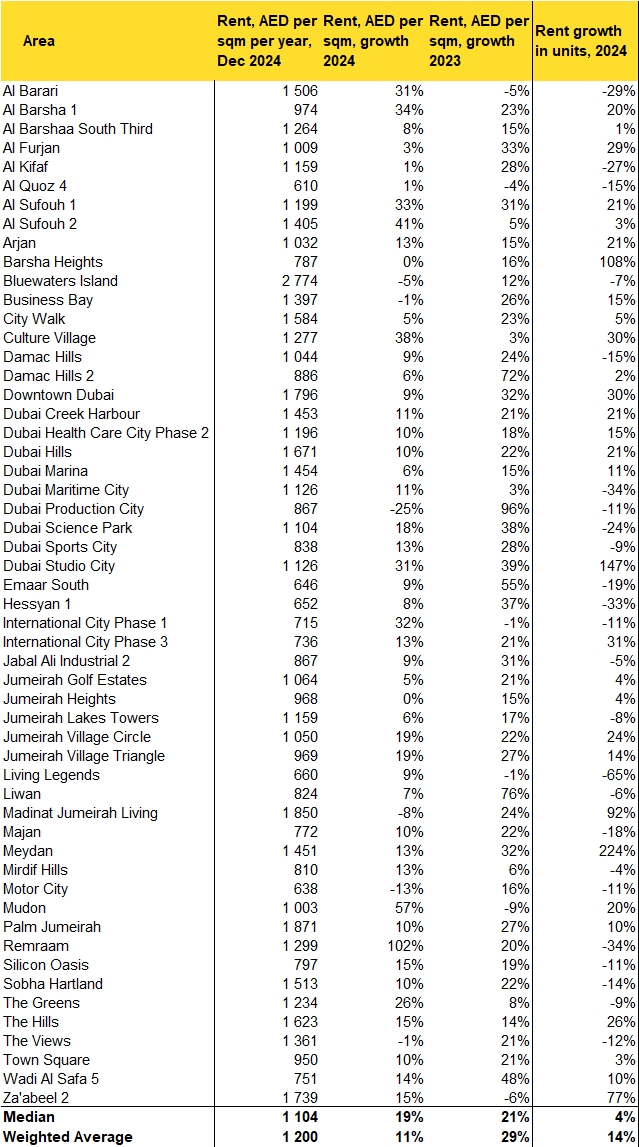

The Dubai residential rental market has seen substantial shifts in 2024, with notable differences across various regions. The weighted average rent price in December 2024 stood at AED 1,200 per square meter per year, reflecting an 11% increase compared to the previous year. Despite a general increase in rental prices, the median rent of AED 1,104 per sqm indicates that some areas have experienced higher-than-average growth, while others have seen declines or stagnation.

The rental price growth rate in 2024 (11%) is lower than in 2023 (29%), suggesting a market that is stabilizing after an exceptionally strong previous year. Rent volume growth in 2024 stands at 14%, indicating sustained demand but at a more moderate pace compared to the earlier surge in 2023.

Here we provide insights about Dubai’s apartment rental market in 2024, examining key trends, area-specific movements, and projections for 2025.

Key Rental Market Trends in 2024

Luxury Neighborhoods Witness Sustained Growth, but at a Slower Pace

Dubai’s high-end residential communities continued to attract tenants, but price appreciation in some prime areas has started to decelerate. Rental prices in Palm Jumeirah (+10%), Downtown Dubai (+9%), and Dubai Marina (+6%) recorded moderate increases. However, transaction volumes varied across these locations. Downtown Dubai, known for its proximity to major business hubs and luxurious lifestyle, saw rental transactions rise by 30%, driven by corporate leases and long-term expatriate commitments. Meanwhile, Palm Jumeirah experienced more muted demand growth, suggesting a potential plateau in ultra-luxury rental demand. Dubai Marina remained a preferred location for professionals, but rent price increases were slower compared to other segments.Mid-Tier and Affordable Neighborhoods Outperform in Rental Growth

Areas catering to mid-income residents showed stronger rental growth compared to premium districts. Several factors contributed to this trend, including affordability, availability of modern amenities, and increasing preference for community-style living.- Al Barsha 1 (+34%), Culture Village (+38%), and International City Phase 1 (+32%) witnessed robust rental price growth.

- Jumeirah Village Circle (+19%) and Remraam (+102%) saw significant rental demand, particularly among young professionals and families looking for budget-friendly alternatives.

- Dubai Studio City (+31%) emerged as an attractive destination for tenants, thanks to its mix of affordability and accessibility to commercial districts.

Declining Rental Demand in Certain Areas Despite Price Growth

While many areas enjoyed strong rental price appreciation, certain neighborhoods faced declining demand. In Al Barari (+31%), Al Furjan (+3%), and Dubai Production City (-25%), rental transactions dropped significantly. This trend indicates that rental price hikes in some areas may have reached a point where they deter potential tenants, causing landlords to face longer vacancy periods.Market Corrections in Select Locations

Some areas witnessed a slowdown in rental price growth or even declines, driven by oversupply or shifting tenant preferences:- Motor City (-13%), Dubai Production City (-25%), and Madinat Jumeirah Living (-8%) recorded negative rental growth.

- These trends suggest a possible correction in rental rates in previously high-demand areas, as new supply enters the market and tenants explore alternative options.

Rapid Growth in Emerging Residential Hubs

Newer residential communities gained traction in 2024, with demand shifting towards areas offering modern infrastructure at competitive prices.- Remraam (+102%) led rental price growth, fueled by affordability and improved connectivity.

- Jabal Ali Industrial 2 (+9%) and Dubai Science Park (+18%) attracted strong tenant interest, particularly from professionals working in adjacent commercial zones.

Factors Influencing Dubai’s Rental Market in 2024

Economic Growth and Population Increase

Dubai’s economic expansion, driven by sectors such as finance, tourism, and technology, has contributed to rising demand for rental properties. The influx of expatriates seeking employment opportunities has further boosted demand, especially in mid-tier rental segments.Interest Rate Trends and Mortgage Market Impact

Higher global interest rates in 2024 have influenced property purchasing decisions, leading more residents to opt for renting rather than buying. This has added pressure on rental prices, particularly in popular residential districts.Supply and New Project Deliveries

Several new apartment developments were completed in 2024, affecting rental price trends. While areas with significant new supply, such as Dubai Hills and Madinat Jumeirah Living, experienced moderate rental adjustments, others with limited new inventory maintained high price growth.Changing Tenant Preferences

Post-pandemic lifestyle changes have led tenants to seek larger living spaces, outdoor amenities, and community-focused developments. This has benefited areas like Jumeirah Village Circle, Dubai Studio City, and Remraam, which offer modern, spacious units at competitive rates.Outlook for Dubai’s Apartment Rental Market in 2025

Continued Growth but at a Moderated Pace

Rental price increases may slow down in some areas as affordability concerns grow. Prime districts such as Downtown Dubai, Palm Jumeirah, and Dubai Hills could see stabilization, while mid-tier locations like Jumeirah Village Circle and International City may continue outperforming in terms of rental demand.New Supply to Impact Rental Pricing

The influx of newly completed apartment projects in 2025 is likely to introduce more competitive rental pricing, particularly in areas with high supply levels. Tenants may benefit from greater choices, leading to potential rent stabilization in oversupplied districts.Increased Tenant Migration to Affordable Areas

As rental prices rise in established districts, tenants are expected to continue moving toward emerging communities such as Dubai South, Dubai Studio City, and Remraam, where they can find better value for money.Higher Demand for Flexible and Furnished Rentals

With Dubai’s growing gig economy and an influx of short-term residents, demand for furnished and short-term rental properties is likely to rise in 2025. This trend could drive rental price premiums in key business and tourist-friendly locations.Regulatory Adjustments and Market Stability

The Dubai Land Department (DLD) and Real Estate Regulatory Agency (RERA) are expected to introduce new measures to ensure a balanced rental market. Rent control mechanisms and enhanced tenant protections may play a larger role in stabilizing rent fluctuations.Note: 2024 data is for the full year (January – December 2024)

Tags: Rents

Property Makler © 2026 Contacts T&C About