|

Property Makler

Advanced analytics for residential real estate investing |

|

Dubai, UAE US |

Dubai US Market Research

Dubai apartment rental market in H1 2024 - A landscape of growth and stabilization

16 Jul 2024

Key points

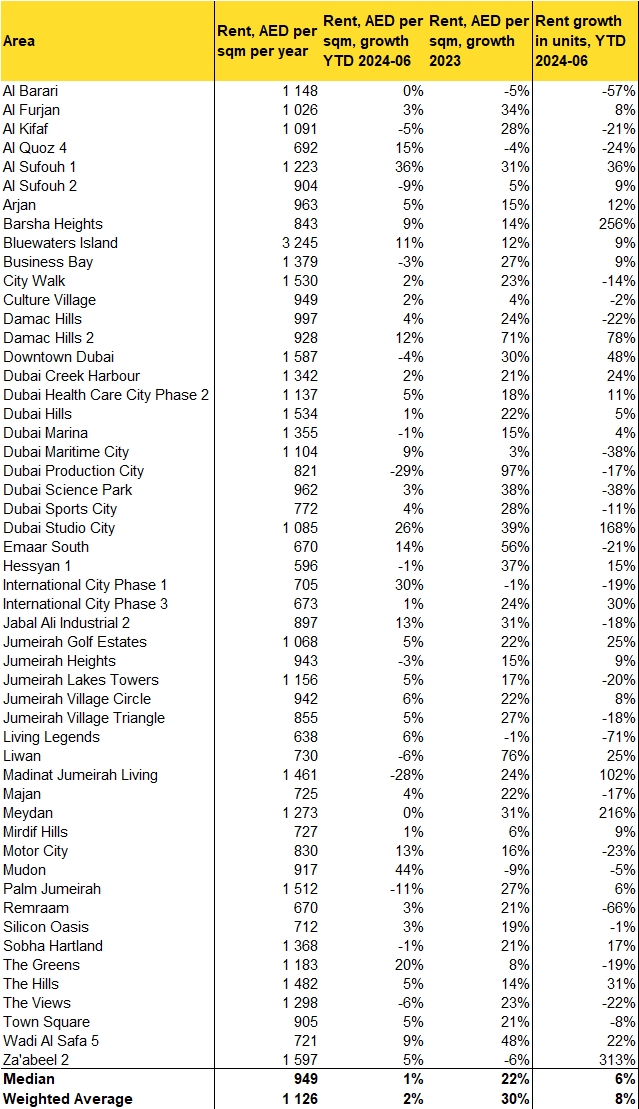

- Overall rental growth in 2024 has moderated to 2% YTD, a significant slowdown from the 30% growth seen in 2023, indicating a stabilization of the market.

- Areas like Al Sufouh 1, Mudon, and Emaar South have seen substantial rental rate increases, reflecting strong demand and ongoing infrastructure development.

- In contrast, regions like Dubai Production City and Madinat Jumeirah Living have experienced sharp declines in rental rates, possibly due to oversupply or shifting tenant preferences.

- The market outlook for the remainder of 2024 suggests continued moderation in rental growth, with the potential for further stabilization as supply catches up with demand.

Market dynamics in H1 2024

As of June 2024, the Dubai residential apartment rental market reflects a mixed bag of trends, with rental rates varying significantly across different areas. The data showcases the complexity of the market, with some regions experiencing substantial growth in rental prices, while others have seen declines, pointing to a highly segmented market influenced by various factors such as location, demand, and the availability of new developments.Several areas have recorded impressive increases in rental rates per square meter year-to-date (YTD), highlighting strong demand in these locales. They behave like strong rental hotspots.

- Notably, Al Sufouh 1 has seen a remarkable 36% increase in rental rates YTD, signaling its growing appeal as a residential destination.

- Mudon and Emaar South also stand out with significant rent increases of 44% and 14% YTD, respectively.

- The Greens also stands out with a 20% YTD increase, following a more modest 8% growth in 2023.

On the other hand, some regions have witnessed declines in rental rates, suggesting potential challenges such as oversupply or shifting tenant preferences. For example, Dubai Production City has seen a sharp 29% decline in rental rates YTD, while Madinat Jumeirah Living experienced a 28% drop. These decreases could indicate a cooling demand or an oversaturated market in these areas, leading landlords to lower rents to attract tenants.

The overall market trends indicate a moderate weighted average growth of 2% in rental rates YTD, which is relatively stable but notably lower than the 30% growth observed in 2023. This suggests that while the market is still growing, the pace has slowed considerably compared to the previous year, reflecting a possible stabilization after a period of rapid rent increases.

Moreover, certain areas have shown resilience and steady rental growth, underscoring their enduring attractiveness to tenants. Areas like International City Phase 1 and Jumeirah Golf Estates have seen rental increases of 30% and 6% YTD, respectively. These areas, known for their affordability and well-established communities, continue to attract a steady stream of tenants, contributing to their sustained rental growth.

On the flip side, other prominent areas such as Palm Jumeirah and Downtown Dubai have seen rental rates decline by 11% and 4% YTD, respectively. These decreases may be due to an influx of new supply or tenants shifting preferences towards newer or more affordable developments in other parts of the city.

Comparison with 2023

When comparing the year-to-date (YTD) rental growth in 2024 with the rental growth experienced throughout 2023, a noticeable trend of moderation becomes evident in the Dubai residential apartment market.In 2023, the rental market saw significant increases, with a weighted average growth of 30% across Dubai. This sharp rise was indicative of a booming market, driven by strong demand, limited supply in certain areas, and a post-pandemic rebound that spurred both rental and real estate markets.

However, as of June 2024, the YTD rental growth has slowed considerably, with a weighted average increase of just 2%. This stark contrast between the two periods suggests that the market is stabilizing after the rapid escalation in rents seen in 2023. Several factors could be contributing to this deceleration:

- Market Saturation: After the significant price increases in 2023, the market may be experiencing saturation in some areas, where rental rates have reached a point that has reduced the rate of increase in tenant demand.

- Increased Supply: The influx of new developments and ready properties coming onto the market may be providing tenants with more options, thereby easing the pressure on rental rates that was evident last year.

- Economic and Regulatory Factors: Any shifts in the broader economic environment, such as inflation or changes in employment patterns, as well as regulatory measures aimed at stabilizing the market, could also be playing a role in tempering rental growth.

Dubai residential apartment rental market outlook

As we look ahead to the remainder of 2024, the Dubai apartment rental market is expected to continue navigating a path of stabilization, with growth rates likely to moderate further as the market adjusts to the evolving economic and demographic landscape.The slowdown in rental rate increases seen in the first half of the year suggests that the market may be reaching a more sustainable equilibrium between supply and demand. As new developments come online, especially in key areas that have already experienced sharp rent increases, the influx of additional units could exert downward pressure on rental rates. This might particularly affect areas like Al Sufouh 1 and Mudon, where rents have surged significantly YTD. However, these areas could still maintain their appeal if they continue to offer high-quality living spaces and amenities that align with tenant preferences.

On the other hand, areas that have seen declines in rental rates, such as Dubai Production City and Madinat Jumeirah Living, may face continued challenges unless demand picks up or supply constraints ease. Landlords in these regions may need to remain flexible on pricing or enhance the attractiveness of their offerings through upgrades or better management practices to draw in tenants.

The trend towards ready properties, as evidenced by the decreasing proportion of off-plan sales, could also influence the rental market. Tenants may increasingly prefer established communities with immediate occupancy, which could benefit areas like International City Phase 1 and Jumeirah Golf Estates, where rental growth has been steady, and demand remains robust.

Moreover, external factors such as changes in interest rates, inflation, and economic conditions in Dubai and the broader region will play a crucial role in shaping rental dynamics. Should the economy remain stable with continued job creation and population growth, we could see consistent demand for rental properties, supporting rental prices. However, any economic downturn or significant rise in the cost of living could dampen rental demand, especially in higher-end segments.

Overall, while the pace of rental growth is likely to remain subdued compared to the rapid increases of previous years, the market is expected to remain resilient. Investors and landlords who adapt to shifting market conditions and tenant needs will be best positioned to navigate the remainder of 2024 successfully.

Dubai residential apartment rental market as of H1 2024 is characterized by both growth and decline across different regions. While some areas continue to see robust demand and rising rental rates, others are experiencing downward pressure on rents, possibly due to oversupply or changing tenant preferences. The overall moderation in rental growth compared to 2023 suggests a market that is moving towards stabilization, with a more balanced dynamic between supply and demand. As the market continues to evolve, it will be crucial for landlords, investors, and tenants to stay attuned to these trends to navigate the complexities of Dubai's rental landscape effectively.

Note: YTD is year to date (January – June 2024)

Tags: Rents

Property Makler © 2026 Contacts T&C About